GOODBYE 2023. HELLO 2024!! WELL, WE HOPE SO AT LEAST.

Most players in the freight market were very happy to see 2023 pass and fade away in the rear view mirror . What a crazy, depressing, flipped upside down market it was. The likes of which haven't been seen in decades and many thought they would never see again. If you were a new broker or carrier who entered the industry during the COVID boom, you were just taught a very valuable lesson; what goes up must come down! And HARD.

Everyone understands the transportation market is very cyclical and has seasons that change the ebb and flow. But what we all just witnessed (and hopefully survived) was a market unlike any other. COVID created a period of glutton; rates were astronomical, shippers were bulging at the seams with freight, and new carriers were welcomed with open arms - and large books of business.

Too big to fail. Too much investment money to fail. Too established to fail. All wrong answers for the freight gods and punish they do. Here we are wrapping up Q1 of 2024 and we are still counting the bodies.

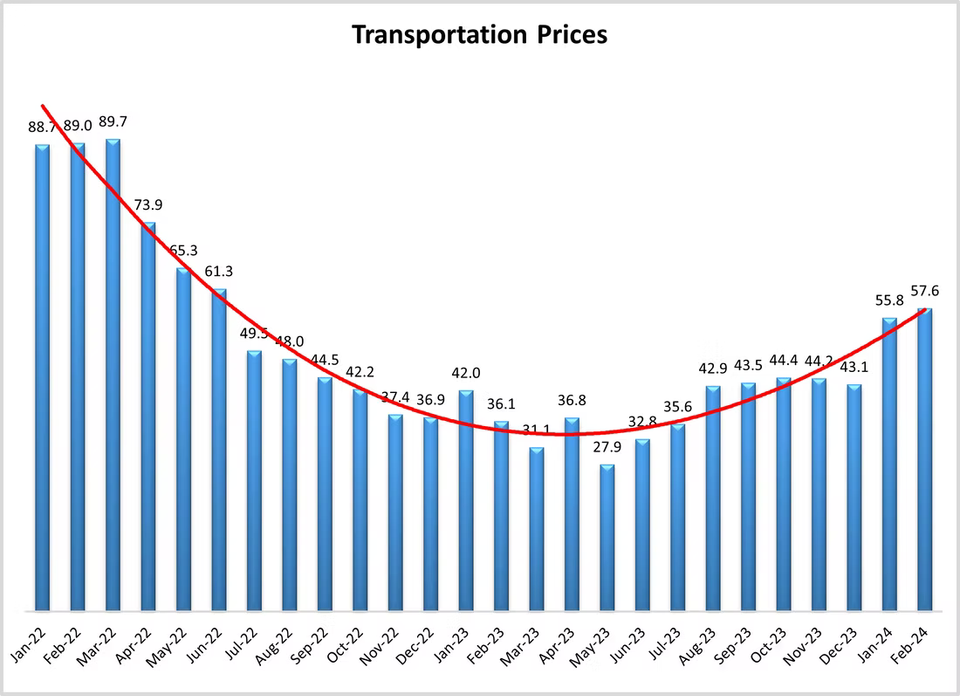

June 2022 was the last time the Transportation Price Index (The LMI) posted a number like 57.6. A hint of an acceleration out of the darkness of the freight recession??? February's TPI of 57.6 was a 0.9 point increase of January 2024, potentially signaling better days to come. Inventory levels, warehouse utilization, transportation capacity and utilization, and transportation prices all showed growth increasing at an increasing rate. Transportation prices growth rates are the highest they have been since the beginning of the freight recession in June of 2022. February was the sixth time in the last seven months that the LMI has reflected growth. These numbers have the Upstream Transportation Index (60.9) to thank as it reflects that manufacturers and wholesalers are starting to move inventory, all while the Downstream Index (52.7) is reflecting a slower rate of price increases for retailers.